For many Canadian businesses, the Scientific Research and Experimental Development (“SR&ED“) program can provide valuable tax incentives. However, businesses claiming SR&ED Investment Tax Credits (“ITCs”) often face uncertainty surrounding eligibility.

In many cases, businesses invest significant time and money into research and development projects without knowing whether the Canada Revenue Agency (“CRA“) will ultimately accept their claim.

For startups and growing companies, this uncertainty can create cash flow and budgeting concerns, particularly where anticipated SR&ED ITC cash refunds are being relied upon to fund future growth.

A bigger, more accessible SR&ED program: What the Federal Budget changed

The calculus just shifted. Recent Federal Budget changes suggest that the SR&ED program is evolving in two parallel ways: first, by expanding the scope of the incentives themselves, and second, by introducing administrative tools (like the pre-claim approval process discussed below) intended to reduce uncertainty for claimants.

More money on the table: What the financial enhancements actually mean

From a financial perspective, several changes have been introduced to increase both the amount of expenditures eligible for the enhanced refundable SR&ED credit, and the ability for businesses to access refundable credits:

| Change | Summary | Practical Impact |

| Increased enhanced expenditure limit | The annual expenditure limit for the 35% refundable SR&ED ITC has been increased from $3 million to $6 million. | A qualifying company may now generate up to $2.1 million in refundable credits annually, significantly increasing available cash flow if the company has insufficient taxable income. |

| Expanded access to enhanced rate | Certain “eligible Canadian public corporations” can now access the 35% refundable ITC amount (previously limited to Canadian Controlled Private Corporations), subject to revenue-based criteria. | Broadens eligibility to a wider group of innovation-driven businesses, particularly in capital-intensive sectors. |

| Higher phase-out thresholds | For CCPCs, the prior year taxable capital thresholds at which the annual expenditure limit to earn the enhanced SR&ED ITCs begins to be reduced has increased from a range of $10 million to $50 million of taxable capital, to a revised range of $15 million to $75 million. For eligible Canadian public companies, the annual expenditure limit is reduced if average gross revenues for prior years exceeds $15 million and is eliminated once these revenues exceed $75 million. For CCPCs, they can elect to use a revenue threshold in lieu of a taxable capital threshold for the annual expenditure limits. | Allows a larger pool of mid-sized companies to retain access to enhanced refundable SR&ED ITC benefit. |

| Capital expenditures | An amount equal to 40% of capital expenditures on the acquisition cost of depreciable property used in SR&ED activity are eligible for the refundable ITC at the ITC rate of 35%. In addition, the capital expenditure would be eligible for an immediate expense deduction. | Cash refundable ITCs are available for a portion of the capital expenditures on depreciable property. |

In particular, the enhanced refundability rules for ITCs may be significant for many taxpayers, as they expand the pool of companies that can rely on SR&ED as a source of near-term cash flow, rather than simply a reduction of taxes payable.

The new pre-claim approval process: Get a yes before you spend

While the financial enhancements above increase the value of the SR&ED program, they do not address a long-standing issue with the program: uncertainty around whether a particular project will ultimately qualify. It is in this context that the CRA’s new pre-claim approval process becomes relevant.

In response to these concerns, the CRA recently launched a new optional “Pre-claim approval process” for eligible SR&ED claimants. This new process officially came into effect on April 1, 2026, and is intended to provide qualifying businesses with earlier certainty regarding the eligibility of planned SR&ED projects.

How it works

a. What is the new Pre-claim approval process?

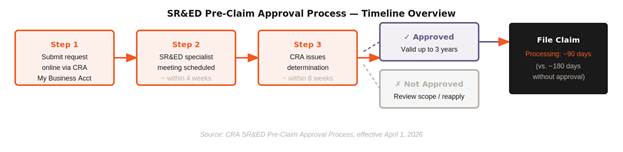

Under the new program, eligible businesses can request that the CRA review a proposed SR&ED project before the work begins, or before substantial costs are incurred. If approved, the CRA will provide a pre-claim approval determination confirming that the project appears to qualify for SR&ED tax incentives, based on the information submitted.

According to the CRA, businesses that receive pre-claim approval may also benefit from faster processing timeline once the SR&ED claim is ultimately filed. For example, when a claim only requires an expenditure review, the CRA has stated that processing times may be reduced from approximately 180 days to only 90 days.

The CRA has indicated that this process is intended to provide early certainty, streamline the SR&ED application process, and create a more direct relationship between claimants and CRA reviewers.

b. Who can apply?

Currently, the program is targeted primarily at startups and smaller businesses. To qualify, businesses must generally:

- Be a Canadian-controlled private corporation, Canadian corporation, or Canadian partnership;

- Have annual gross income of less than $25 million; and

- Be in good standing with the CRA.

Businesses can request pre-claim approval for up to three projects at a time.

The application process involves:

- Opening a pre-claim approval request online;

- Submitting supporting information through CRA My Business Account;

- Meeting with an SR&ED specialist, typically within four weeks of submitting your application; and

- Receiving a determination from the CRA, typically within eight weeks of submitting your application.

If approved, the determination may remain valid for up to three years.

c. Why this matters for your business

For businesses investing heavily in research and development, this new process may help reduce the uncertainty surrounding whether a project actually qualifies. This new process gives qualifying businesses an opportunity to engage with the CRA earlier in the lifecycle of a project.

This new process may also help businesses prepare stronger documentation from the outset. Early CRA engagement may help businesses better understand what records and support will be required if a claim were to be subsequently audited.

d. What pre-claim approval doesn’t cover

While this new pre-approval process may provide greater certainty, businesses should not assume that pre-claim approval guarantees that a future SR&ED claim will be accepted in full.

The CRA has stated that claims involving pre-approved projects may still be selected for review, particularly where:

- The actual work differs significantly from the approved project description;

- Expenditures appear inconsistent with the approved activities; or

- The claim includes additional projects that were not pre-approved.

In addition, pre-claim approval appears to focus primarily on whether the proposed project itself may qualify as an SR&ED, rather than whether all of the associated expenditures will ultimately be accepted by the CRA. Businesses will therefore still need to maintain detailed records supporting salaries, contractor payments, materials, and other claimed expenditures.

Important limitation

Pre-claim approval is not a guarantee that a future SR&ED claim will be accepted in full. The CRA can still select pre-approved claims for review if actual work deviates from the approved description, expenditures appear inconsistent, or the claim includes projects that were not pre-approved.

Key takeaways for revised SR&ED process

A larger group of companies are now eligible for refundable SR&ED ITCs, and the thresholds at which the refundability is available have been increased.

However, businesses considering the new pre-approval process should keep the following in mind:

- Strong project descriptions remain critical. The CRA will still expect businesses to clearly explain the technological uncertainty and experimental development involved in the project.

- Documentation should begin early. Records, testing results, design iterations, and project notes remain important, even when pre-claim approval is obtained.

- Not all projects will qualify. The SR&ED program is intended to support work involving scientific or technological uncertainty. For example, simply upgrading software or customizing an existing product may not qualify for SR&ED tax incentives.

The CRA’s new SR&ED pre-claim approval process represents a significant shift in how qualifying businesses may interact with the SR&ED program going forward. For eligible businesses, the ability to obtain early feedback from the CRA before major costs are incurred may improve planning, reduce uncertainty, and potentially accelerate access to SR&ED tax incentives.

That said, pre-claim approval is not a shortcut. Strong documentation, accurate project descriptions, and careful tracking of expenditures remain as important as ever. The new process is a planning tool, not a guarantee. If your business is investing in R&D and you are not sure whether your projects qualify, or whether the new financial thresholds change your position, now is the time to find out.

If you have any questions about this new SR&ED pre-claim approval process, or the enhanced ability to qualify for a cash refund of the SR&ED ITCs, please contact a lawyer from our Corporate Tax Group.

{kind=link}